TRUMP Accounts

A new type of tax-advantaged savings accounts for children officially opened for contributions on July 4, 2026 — and if you have kids or grandkids under 18, it may be worth a close look. Here's a plain-English breakdown of how TRUMP Accounts work, who they're right for, and how they compare to strategies you may already be using.

What Is a TRUMP Account?

TRUMP Accounts — created under the Working Families Tax Cuts Act (part of the "One Big Beautiful Bill" signed into law in 2025) — are tax-deferred savings accounts designed for children under 18. Think of them as a hybrid between a traditional IRA and a children's savings account. Contributions go in after-tax, grow tax-deferred, and the account converts into a standard traditional IRA when the child turns 18.

Key fast facts:

Available starting July 4, 2026

Annual contribution limit: $5,000 (indexed for inflation after 2027)

Any U.S. citizen child under 18 with a Social Security number is eligible

The federal government seeds $1,000 into accounts for children born January 1, 2025 – December 31, 2028 — at no cost to the family

How Contributions Work?

Anyone can contribute to a child's TRUMP Account — parents, grandparents, family friends, or even employers. The combined total from all sources cannot exceed $5,000 per year. Employer contributions are capped at $2,500 and count toward that $5,000 ceiling. Contributions from qualifying charitable organizations and government entities are exempt from the annual cap.

Contributions are not tax-deductible. Unlike a traditional IRA or 401(k), you don't get a deduction for putting money in. The benefit is entirely in the tax-deferred growth — no taxes owed on dividends, interest, or gains while the money stays in the account.

Where the Money Is Invested?

During the child's growth period (birth through age 17), TRUMP Account funds must be invested in a diversified U.S. stock index fund that minimizes fees. There is no flexibility here — this is set by law. If you want control over investment selection, a custodial brokerage account (UTMA/UGMA) or a 529 with broad fund options may be better suited to your goals.

When Can the Money Be Accessed?

This is critical to understand. No withdrawals are permitted before January 1 of the year the child turns 18 — no exceptions except death, rollovers, or returning excess contributions.

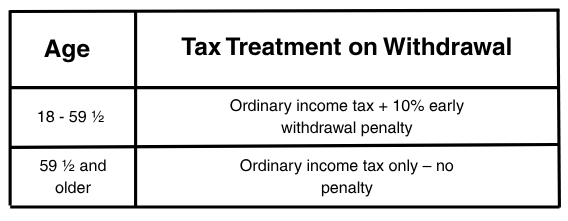

Once the child turns 18, the TRUMP Account automatically converts into a traditional IRA:

Penalty-free exceptions (same as a traditional IRA) include: first-time home purchase (up to $10,000), qualified higher education expenses, total and permanent disability, death, unreimbursed medical expenses exceeding 7.5% of AGI, and substantially equal periodic payments (SEPP).

Corporations & Philanthropists?

Employers may choose to contribute to the Trump Accounts for their workers or their workers' children, supporting early savings and financial readiness. Employers may choose to offer employees a salary reduction program under a "cafeteria plan" so that employees can make pre-tax contributions to Trump Accounts.

Corporations can contribute up to $2,500 to Trump Accounts on behalf of their employees' children. All contributions are tax-deductible.

Nonprofit organizations and local governments can contribute to Trump accounts of all children in a state or qualified geographic area.

Who Should Consider a TRUMP Account?

TRUMP Accounts make the most sense if:

You want to give a child or grandchild with no earned income a head start on retirement savings

The child was born between 2025–2028 and qualifies for the free $1,000 government deposit

TRUMP Accounts may not be the right fit if:

You're saving specifically for college — a 529 offers better flexibility for education expenses

The child has earned income and is eligible to contribute for a Roth or Traditional IRA.

You want investment flexibility beyond a passive index fund

Our Take at Merited Wealth?

TRUMP Accounts are a new tool in the financial planning toolbox — and like most new tools, context is everything. The free $1,000 government contribution for recent births is a no-brainer if your child or grandchild qualifies. Beyond that, whether TRUMP Accounts belong in your strategy depends on what you're already doing, your tax situation, and your timeline.

If you're a high earner who has already maximized your own retirement accounts and wants to do something meaningful for the next generation, this is worth a conversation. For grandparents looking to leave a lasting legacy, TRUMP Accounts offer a simple, structured option.

The accounts open July 4, 2026. If you want to position a child ahead of that date or understand how TRUMP Accounts interact with other planning strategies you already have in place, reach out.